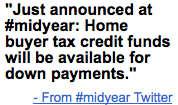

On Tuesday morning I woke up and read a Tweet on Shaun Donovan, Secretary of HUD, announcing that first time buyers could now access their $8000.00 tax credit in the form of a bridge loan and use it towards their down payment on the house they were buying.

I went to NAR press release and read the posted the comment from his speech at the Pre-NAR conference, The Real Estate Summit, advancing the U. S. economy.

Later that day, I received an email from the Michigan Association of Realtors with the same announcement.

As the day went on I received an email from Keller Williams, Ann Arbor saying the same thing. Later that day, one of my team members sent me and email saying she was sending out the BIG ANNOUNCEMENT to all her first time home buyers.

I posted all about the announcement here and then a few lenders said they smelled a fish. I thought to myself, oh they just haven’t got their Mortgagee Letter yet because no way would NAR, MAR and KW say this.

Problem

The problem is this announcement was not going to happen (yet) and the Pre-Published speech of Mr. Donovan was gone from the HUD web-site.

It is still up on the NAR site and I have had no retraction from MAR.

The Dilemma

The point I am making is not to stir the pot again. But, to ask how and why was this ever allowed to be published?

- Why is it still on the Realtor.org site?

- Why no recanting from MAR?

We know the effect social media can have on getting the word out and the speed at which it can happen. My frustration is that reading from three credible sources that their is a new rule FHA rule for first time home-buyers only to have it vanish in a New York minute.

Credibility

When we blog, we put our credibility on the line. Oh it is easily corrected on Activerain but what about the consumers who get the information from an RSS feed or search the $8000.00 tax credit read a post, announcing they can use the $8000.00 tax credit up front for a down payment. (this has been my most searched term since Feb.)

One of my own lenders called the HUD office in Chicago and was told, “Well, it is going to happen, Shaun Donovan announced it, but the details are just not worked out so the speech shouldn’t have been published.” She told her she had pulled it off the HUD site, printed it, then came back after lunch and it was gone. She too had been getting lots of calls from lenders on it wanting more details.

Having attended big conferences I know the leadership likes to announce new things first to a receptive audience before it hits the public. It gets a warm welcome and everyone is happy, happy.

I am just bummed that when we blog, think we have credible sources and then have it blow up in our faces. Are we to accept that with the speed of the internet things just might not be 100% truthful? What happened?

I want to believe I can trust my trade organizations to print the truth the whole truth and nothing but the truth.

The thing is I believe they did publish the truth about what Mr. Donovan said, and news like this spread like wild fire. Hungry Realtors were thrilled with the announcement.

Then the message disappears and like a commenter on my blog said:

“Your trade associations have the credibility of Nancy Pelosi. They told us QUARTER AFTER QUARTER AFTER QUARTER in 2004, 2005, 2006 & even 2007 that the worst is over in the real estate markets. LOL!!!!”

Alex

May 15, 2009 at 11:02 am

I think the advent of Twitter has made other news sources very jumpy. It’s tough to resist the urge to write about something that was literally just announced. The problem is that Twitter only allows 140 characters, so using it as a source is sketchy at best.

Hopefully either the Twitter fad will die out or reporters will get more mature about using it.

Jack Lewitz

May 15, 2009 at 11:31 am

Missy,

I talked with a mortgage broker yesterday about access to the $8,000.00 prior to closing and he said it was a mistake. Who ever put this out in the press did so without thinking about the repercussions because if the money is given to the buyer it would have to be in the form of a “bridge loan” and it would cost the buyer more money.. Good post..

Tim Epps

May 15, 2009 at 12:56 pm

Missy,

Great post and perspective. We all get excited when new opportunities exist to help buyers. However, as industry experts, we must perform due diligence on news we receive. When I first heard about this, my first thought was whether any lenders were on board yet. Secretary Donovan’s statement about this was not even that it was ready – just that they intended to approve it. Yet it was heralded as a done deal.

Jack Lewitz is correct in his comment from a mortgage broker – how would the bridge loan be structured? Just because HUD/FHA will allow it does not mean the market will accept it. FHA does not have a credit score requirement, but most lenders will not approve anything for a borrower with less than a 620 mid-score.

I disagree with Alex about his desire to see Twitter die out (baby with the bath water?). His alternative of reporters (read: all tweeps stating or retweeting facts) should be more responsible. All of us want to do what we can to help bring out the good news in our industry. Premature tweeting only brings out confusion. It doesn’t help when no trade group website or reputable news organization website seems to be able to publish a retraction, an update or pull down the original item. The National Association of Home Builders (NAHB) posting is still on their website ( https://cli.gs/ZAXa1T ) as with Builder magazine who still has their article up ( https://cli.gs/zB6126 ). At least HUD figured out how to pull theirs down ( https://cli.gs/G4XXp1 ). I guess we should expect a governmental agency to be expert at covering up/shredding/rescinding. They are also experts at trial balloons which may have been the point all along.

My concern now is that since this scent has been placed in front of buyer’s noses, will they sit on the sidelines until it becomes fact? This could cause a slow down in that case rather than providing a stimulus to the market. Can it even be implemented in time before the credit to run out?

English fundamentalist Charles Haddon Spurgeon said, “A lie will go round the world while truth is pulling its boots on.” We would all do well to remember this.

Matt Carter

May 15, 2009 at 1:20 pm

Secretary Donovan’s announcement — that HUD will allow first time homebuyers to “monetize” the tax break by pledging it as collateral to obtain a bridge loan from FHA-approved lenders, HUD-approved nonprofits, and state and local housing authorities — remains live on HUD’s site.

https://www.hud.gov/news/speeches/2009-05-12.cfm

Donovan said:

“We all want to enable FHA consumers to access the tax credit funds when they close on their home loans so that the cash can be used as a downpayment,” and he said FHA would soon publish details on its policy allowing the practice shortly.

I understand the FHA letter to mortgagees that spelled out how this was to work was quickly withdrawn — sounds like they may have issues to work out with the IRS.

But a HUD spokesman assured me yesterday that “the details will be forthcoming.” NAR says it’s expecting a formal announcement next week.

Nobody is retracting the story because the original source of information was HUD, and HUD continues to maintain that it is going to implement this policy.

Matthew Rathbun

May 15, 2009 at 3:39 pm

Did KW retract?

I am not sure that the real issue here is that information gets out too fast, but that even the Secretary of HUD doesn’t know what he’s talking about. I think it’s indicative of all the other mis-information about the mortgage issues on a Federal level.

Louise Scoggins

May 15, 2009 at 4:03 pm

I got an email blast from my lender this afternoon in regards to this exact matter. In his email he said the details have not been released as to which banks will be approved for the “short term loan” of the $8,000 to the buyer. It will be very interesting to see how this one plays out over the next couple of weeks.

Matt Stigliano

May 15, 2009 at 4:23 pm

Missy – Have you seen my latest on ActiveRain – the mistakes get deeper.

Matthew Rathbun

May 15, 2009 at 4:31 pm

Matt: Gotta link?

Matt Stigliano

May 15, 2009 at 4:36 pm

Matthew – Yeah…I meant to put it in there…

https://activerain.com/blogsview/1077766/nar-you-silly-old-goat-why-would-you-let-this-be-emailed-to-every-realtor-after-yesterday-

Matthew Rathbun

May 15, 2009 at 4:40 pm

Benn Martin has some more information about this at VARBuzz.com https://tinyurl.com/qfds7n

Missy Caulk

May 15, 2009 at 4:45 pm

Matthew did you get the announcement today from NAR? They are still announcing it in the newsletter. If not I can email it to you.

No Matt S. I haven’t been on there since AM.

My lender emailed me the following information as she called HUD Dept in Chicago, they said it is going to happen, details aren’t worked out, announced to soon.

Alex, I saw the tweet, read it on NAR, went and read the prepared speech my Mr. Donovan on HUD site, then got an email from MAR. I would never JUST trust a twit.

Missy Caulk

May 15, 2009 at 4:47 pm

Jack the prepared speech was on the HUD site. He also said it outloud at the conference.

Danilo Bogdanovic

May 15, 2009 at 8:15 pm

Twitter is not a fad nor will it die any time soon. Regardless of whether you’re a Realtor or a reporter, if Shaun Donovan, the Secretary of HUD stands in front of a podium and makes an incorrect announcement out loud in front of thousands of people, the ONLY person to blame is Shaun Donovan and HUD.

I spoke with someone pretty high up the food chain at Suntrust Mortgage – they said that they’re scrambling to figure out how to implement the (now “proposed”) $8K/downpayment program even though it has not been officially implemented.

At this point, I’ll take the word of the person at Suntrust over HUD’s.

Missy Caulk

May 15, 2009 at 9:32 pm

Matt Carter, I do believe you are right, I think he just jumped the gun so to speak.

My lender called HUD in Chicago and they said it was going to happen. I know lenders are working to see how this can be implemented.

We are all holding our breath. Did you read Matt Stigliano’s post on AR?

https://activerain.com/blogsview/1077766/nar-you-silly-old-goat-why-would-you-let-this-be-emailed-to-every-realtor-after-yesterday-

Missy Caulk

May 15, 2009 at 9:33 pm

Danilo, I heard the same thing, they are working on it.

Paula Henry

May 15, 2009 at 11:55 pm

Missy – I’m so glad I was too busy to catch that bit of news as it happened and report on it. It would be too tempting to report it as written and too embarrassing to recant. Oh, NAR! I think everyone just wants to get good news to the media, often before the facts are in.

Unfortunately, we, who bring the news to our clients trust when our National Trade Orginization speaks, or the Secretary of HUD, they will have the facts first.

Joe Loomer

May 16, 2009 at 9:13 am

I think the horse is out of the barn on this one. Very much like the recent IDX debacle, the Social Media circuit will certainly generate the poopstorm that will keep this alive in some fashion. We all probably remember the last few years of hearing about the “100% FHA Loan is coming.” The tax credit is their bailout, they killed the 100%-er, they get it back sideways via the tax credit.

Imagine the VA buyer switching to FHA in order to move in with 3.5% equity vs. -3% ? I’d take a 6%-plus swing in an Augusta-minute! Especially if Uncle Obama transfers you three years later and you have to sell.

Navy Chief, Navy Pride

Missy Caulk

May 16, 2009 at 9:55 am

John, I didn’t know you were a Navy guy. My older son is on the IKE right now, posted on it on Activerain today for Armed Forces Day.

Missy Caulk

May 16, 2009 at 9:58 am

Paula, you had more important things on your mind. 🙂 I don’t blame NAR too much he did say it…and the speech was public.

But, it should have been taken down and not sent out yesterday in the weekly newsletter.

Thanks again for all your hard work.

Pamela Kabati

May 16, 2009 at 2:57 pm

Just wanted to let you all know that I’m following this thread with interest.

As the VP of Publications for NAR, my staff and I are continually talking about how important it is today to be “fast” with our news, to use Twitter to engage with our readers, AND, clearly, to still be accurate.

We hear what you all are saying, and we certainly apologize for any confusion our reporting caused.

Missy Caulk

May 16, 2009 at 3:10 pm

Thanks Pam, appreciate you stopping by.

Matt Stigliano

May 17, 2009 at 1:07 pm

Pamela – I would like to also add my thanks to you for stopping by. Stacey Moncrieff (Editor In Chief, Realtor® Magazine) has stopped by my blog post and I’m seeing a lot of positives to NAR’s work to get involved directly with us on issues that we are talking about. While there are still issues at least there’s communication.

Lani Rosales

May 17, 2009 at 3:03 pm

Missy, your greater point is about dissemination of information, right? Sometimes the bigger the machine, the more gears it has and the slower it is to get the gears to move. Tough spot they’re all in, maybe Monday they’ll get to retractin’ 🙂

Matt Stigliano

May 17, 2009 at 8:00 pm

Lani – While I agree that the bigger the machine, the more gears it has theory, I’m not sure if that should be taken into account. If Microsoft said something false and caused an uproar, you can be sure that they’d be making it right as fast as they could. They have a reputation to keep. And Microsoft is a bad example in a sense, because they’re not the association that everyone turns to for information (ok, maybe not everyone turns to them, but they should be able to be considered a trusted source of news for the Realtor® public). This issue is not just about dissemination, but the continued repetition of info that was known to be inaccurate. Three days later NAR sends the email giving out information that we had been discussing was dead on arrival for days? You and I both know how quick it is to send a mass email to fix a problem. Of course, according to Stacey Moncreiff, they didn’t know about the email until they read my blog, which is a little problematic on it’s own.

I hope we will see a retraction of some sort, since without it, many agents will still not know (not every agent reads 50 gazillion blogs a day) or not believe the blogs about it that have corrected their info.

It is a tough spot and I do enjoy seeing the immediate response of certain members of NAR (much like Todd had discussed recently), but I do think we’ve got a long road ahead of us.

Lani Rosales

May 17, 2009 at 8:39 pm

So with the same analogy, if the biggest gears are unaware that the others are turning (or want to turn), they lack a response. This whole thing is silly, response time shouldn’t be limited to business hours M-F.

Jacob

May 18, 2009 at 10:37 pm

I’m newish to the blog world and trying really hard to play by the rules or at least try to learn them for my own site. Like many others, I want to try to get information out to consumers as quickly and accurately as possible and for me, the NAR news feed, HUD website and other “reputable” sources have always been sort of no-brainers. I posted this news right when it hit but since I couldn’t find any additional information at the time I felt compelled to put up a little disclaimer. Since then I’ve been waiting and watching for more clarification but all I’ve seen so far is this latest at https://www.realtor.org/RMODaily.nsf/pages/News2009051801. Certainly people make mistakes and information can get leaked but I don’t understand the delay in a recant or clarification from any higher up anywhere. I agree with you, Missy, it has left me all bummed out with a blown up face and has definitely made me question my own response time to their news releases as well.

Pamela Kabati

May 19, 2009 at 9:50 am

Just wanted to check back in to let you all know that we published the following story in the REALTOR Magazine Online daily news yesterday and also made this information available from the home page of REALTOR.org.

The bottom line is that HUD intends to allow the monetization of the first-time homebuyer tax credit, but is still working out the details. They’ll spell out these details “shortly,” according to the a HUD spokesperson.

We’re tracking this daily now with HUD and will let you know when the official guidance is released. We’ll tweet about it and will also post to our Speaking of Real Estate blog.

Matt Carter

June 1, 2009 at 11:38 am

The uncertainty about how this would actually work has been resolved with the issuance of the FHA letter to mortgagees on May 29 spelling out the rules.

The bottom line is that the tax credit can be “monetized” and applied to the down payment or to cover closing costs on an FHA-backed loan — but the money can’t be used to meet the FHA’s 3.5 percent minimum down-payment requirement.

See Mortgagee Letter 2009-15.

However, there are state housing finance agencies that offer soft seconds — including some programs that take the borrower’s anticipated tax credit into account as part of the underwriting process — that CAN be applied to FHA’s minimum down payment requirements.

In other words, you can’t use money obtained solely on your expectation that you will be getting this tax credit to FHA’s 3.5 percent minimum down payment requirement. But you can use it to make an additional down payment and for closing costs.

And your eligibility for the tax credit may help you obtain a soft second loan from a state HFA that you can use to meet FHA’s 3.4 percent down payment requirement.

Here are some states that offer first-time homebuyer tax credit loan programs.

https://www.ncsha.org/section.cfm/3/34/2920